Holiday Lets .

Holiday Lets .

The FHL regime has now been abolished. If you owned or purchased a holiday let, your opportunity to maximise capital allowances is time sensitive.

Qualifying relief is not limited to new refurbishments. Fixtures already within the property when you acquired it can generate substantial tax savings, alongside any capital improvements you have made since.

Most accountants focus on invoices for recent spend. A specialist survey identifies embedded assets within the original purchase price as well as qualifying capex that may have been overlooked.

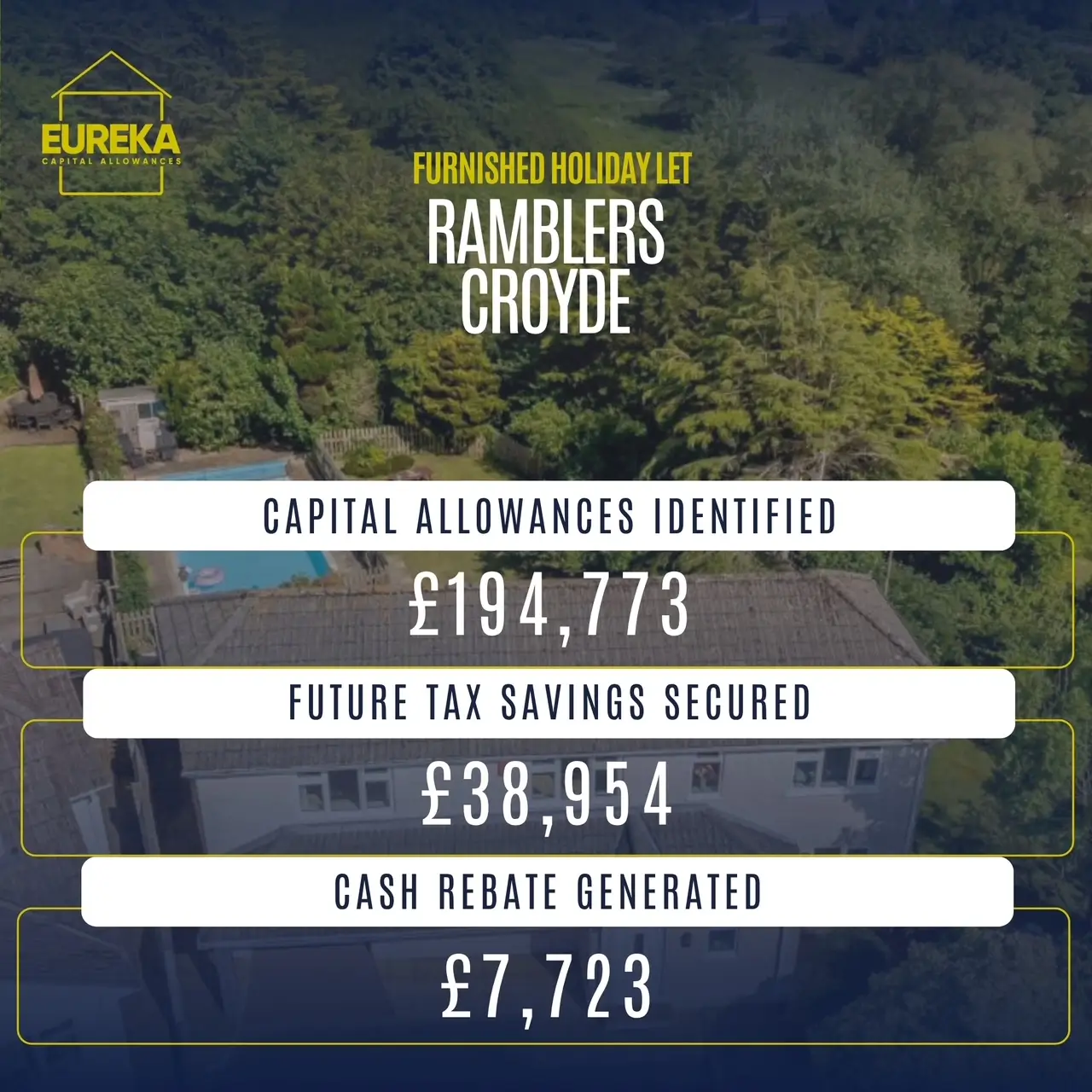

For holiday let claims, 30% of the purchase price can qualify for Capital allowances.

And much, much more…

What can a holiday let owner claim on?

UK legislation allows some business property owners to claim capital allowances on qualifying fixtures already within a property at acquisition, even where these assets were already in place at the time of purchase.

Newly added items and post-acquisition expenditure can also qualify. Whilst accountants typically claim the more obvious items, a surveyor led review can identify additional embedded fixtures and integral features often missed, unlocking further valuable tax relief.

“Eureka helped me realise the potential of capital allowances against my holiday let. They did all the heavy lifting, my job was simply to brief them up front and write the cheque at the end. I doubt I would ever have got near this had they not helped me through it.”

Neil Cross

Ramblers, Croyde

Questions.

Have any questions that we haven’t answered here? Get in touch with us and we will do our best to answer them for you!

Why Accountants Can’t Claim These Allowances.

Capital allowances on property cannot be identified from accounts alone and usually require a specialist review of the building itself. As accountants are not trained or insured to carry out building surveys, significant capital allowances are routinely missed without this process.

What Are Capital Allowances?

Capital allowances allow businesses to deduct qualifying capital expenditure on plant and machinery from taxable profits. When a commercial property is purchased, part of the purchase price may relate to qualifying assets already within the building, which are often overlooked but can deliver significant tax relief when properly identified.

Who Can Claim Capital Allowances?

Businesses and property owners who incur qualifying capital expenditure, including those who purchase commercial property, may be entitled to claim.

What Can Qualify?

Capital allowances generally apply to qualifying plant and machinery and certain fixtures within a commercial property. These items are often embedded within the building and, when correctly identified through specialist analysis, can be pooled and claimed for tax relief.